Case Study 4: How One Florist is Growing Her Property Portfolio with a Discretionary Trust

Meet Sarah*, a successful florist who runs her thriving business through a family trust. With her flower business blooming and generating strong profits, Sarah started thinking about the next chapter: building long-term wealth through property investment—and creating a legacy for her two children.

The Vision: Building a Property Portfolio with Purpose

Sarah’s plan was two-fold:

Start a property portfolio while her business income is strong.

Eventually pass control of these investments to her children—before retirement, and ideally without triggering costly taxes or fees.

That’s when Sarah reached out to Trustify.

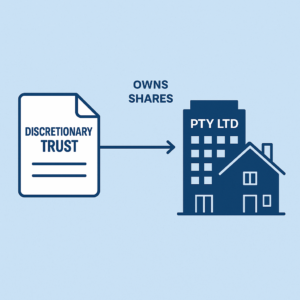

The Solution: A Discretionary Trust (Family Trust) for Property Investment

After speaking with our team and being guided through the various structuring options, Sarah chose to purchase her first investment property through a discretionary trust (commonly known as a family trust).

Why? For Sarah, the benefits made it the clear choice:

✅ Asset Protection – Holding the property in a trust provides a legal separation between her personal assets and investments.

✅ Income Distribution Flexibility – Any rental income or capital gains can be flexibly distributed among family members, which can help with tax planning.

✅ Smooth Succession Planning – When the time comes, Sarah can change control of the trust—by updating key roles like the appointor or trustee—without triggering capital gains tax or stamp duty. This allows her to pass the investment portfolio to her children in a tax-effective way while she’s still alive.

But It’s Not All Roses: The Trade-Offs

Of course, every structure has its trade-offs, and discretionary trusts are no exception.

📌 Higher Land Tax – In many states, properties held in trusts are subject to higher land tax rates.

📌 Ongoing Admin Costs – A trust requires annual accounting, legal reviews, and ASIC fees (if a corporate trustee is used).

📌 Loss Quarantining – Losses in a trust typically can’t be used against other personal income. However, in Sarah’s case, this wasn’t a concern—because she runs her florist business through another trust, she can distribute profits into the property trust to absorb any negative gearing.

The Outcome

Sarah now owns her first investment property in a discretionary trust (family trust), with more planned. She has peace of mind knowing her assets are protected, her legacy can be passed on easily, and her structure supports tax flexibility along the way.

At Trustify, we love helping business owners like Sarah think beyond today—building wealth for tomorrow while staying compliant, protected, and informed.

*Client name changed for privacy.

Disclaimer: This article is for educational purposes only and does not constitute legal, financial, or tax advice. Please seek professional advice tailored to your personal circumstances before making any financial decisions.

Others

-

-

-

-

October 20, 2025 Buying Property Under Your Personal Name in Australia: Pros and Cons

-

October 18, 2025 Service Trust Business Structure in Australia