Buying Property in a Discretionary Trust in Australia: Pros, Cons, and Strategic Insights

As your property portfolio grows, structure matters.

While buying in your personal name may be simple and cost-effective at the start, more sophisticated investors often consider using a discretionary trust — particularly when they want asset protection, tax flexibility, and control over future succession.

In Australia, discretionary trusts are one of the most versatile and widely used structures for owning investment properties. But like all structures, they come with trade-offs — especially when it comes to borrowing power, tax rules, and loss utilisation.

Let’s break down what you need to know before buying property in a discretionary trust.

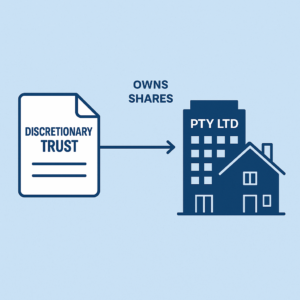

🏦 What Is a Discretionary Trust?

A discretionary trust (often called a family trust) is a legal structure where the trustee holds assets for the benefit of a group of beneficiaries.

Unlike other structures, no one has a fixed ownership interest in the trust.

The trustee has discretion to decide how and to whom the income or capital is distributed each year.

This flexibility provides significant tax planning advantages, asset protection, and succession control, making it a powerful long-term vehicle for property investors.

✅ Advantages of Buying Property Through a Discretionary Trust

1. Strong Asset Protection

One of the biggest reasons investors use discretionary trusts is asset protection.

Because beneficiaries don’t have a fixed interest in the trust’s property, those assets are typically protected from personal creditors.

If a beneficiary or director faces legal or financial issues, the trust’s assets generally cannot be seized — provided the trust has been properly structured and maintained.

This makes discretionary trusts particularly popular among business owners, professionals, and investors wanting to safeguard assets from personal risk.

2. Tax Flexibility and Income Distribution

A discretionary trust allows income to be distributed flexibly among beneficiaries each year — such as to a spouse, adult children, or related entities.

This can help reduce the overall tax burden by directing income to family members in lower tax brackets.

Additionally, capital gains can often be distributed to beneficiaries in a way that optimises access to the 50% CGT discount and other tax offsets.

3. Land Tax Treatment and Threshold Benefits

From a land tax perspective, a discretionary trust is assessed under trust land tax thresholds and rates.

These are generally higher than company rates, though sometimes less generous than individual thresholds, depending on the state.

However, the strategic use of multiple trusts can sometimes help investors minimise overall land tax exposure — particularly once an individual’s threshold has already been exceeded.

For example, if you already own several properties personally and exceed the individual land tax threshold, setting up a separate discretionary trust for new acquisitions may help reset the calculation base.

4. Borrowing Flexibility and Long-Term Leverage

At first glance, borrowing through a trust can appear more restrictive.

Many lenders will apply tighter policies or lower borrowing limits, as the trust structure adds complexity to the loan assessment.

However, some lenders — particularly those familiar with investment structures — will disregard existing trust loans when assessing your personal borrowing capacity, if the trust is trading profitably and supported by proper financial documentation from your accountant.

This means that while borrowing capacity through a trust might be lower upfront, it can actually improve your long-term lending flexibility — because the trust’s financial performance is assessed separately from your personal profile.

5. Control and Succession Planning

A discretionary trust provides excellent flexibility for long-term control and estate planning.

Ownership and management can be transferred or restructured through updates to the trust deed, such as amending the appointor, trustee, or beneficiary classes, without triggering capital gains tax or stamp duty (subject to legal advice and jurisdiction).

This means you can gradually hand over control to the next generation or to key people in your structure without changing legal ownership.

⚠️ Disadvantages of Buying Property in a Discretionary Trust

While the benefits are clear, there are important limitations and risks that need to be understood before committing to this structure.

1. Negative Gearing Limitations

Unlike personal ownership, losses in a trust cannot be distributed to beneficiaries to offset their personal income.

If your property is negatively geared, those losses are trapped within the trust and can only be carried forward to offset future profits.

For high-income earners relying on negative gearing benefits, this is often the biggest drawback of using a discretionary trust.

That said, there are advanced strategies that can help manage this issue — such as hybrid trusts or income allocation arrangements — but these are complex and require specialist advice.

2. Higher Setup and Ongoing Costs

Establishing a discretionary trust with a corporate trustee involves legal and registration costs.

Ongoing expenses include annual tax returns, accounting fees, and ASIC compliance for the corporate trustee.

While these costs are manageable, they need to be factored in as part of your investment planning.

3. Borrowing Can Be More Complex

Not all lenders are comfortable lending to trusts.

Some require personal guarantees from the trustee directors, and others may assess borrowing based on both trust and personal income.

It’s important to work with brokers or banks familiar with trust lending, and to maintain clear financial records.

4. Land Tax Can Still Be Significant

While trusts can help manage land tax exposure, in some states (like NSW and VIC), the trust threshold is lower or surcharges apply unless the trust is specifically registered as a family trust.

Always review state-specific land tax rules before purchasing property through a trust.

🧩 Example Scenario

Let’s take James and Emily, a couple who run a small business and want to invest in property without putting their personal assets at risk.

They establish the J&E Family Trust with a corporate trustee and purchase an investment property through the trust.

-

The trust earns rental income and distributes profits to Emily in a lower tax bracket.

-

Their personal assets remain protected from business liabilities.

-

The trust allows them to adjust distributions each year to suit their financial situation.

-

Their borrowing capacity is slightly lower at the start, but as the trust builds its own income history, some lenders no longer count its debt against their personal borrowing power.

This structure gives them long-term flexibility and control, at the cost of slightly higher initial setup and accounting complexity.

🧭 When a Discretionary Trust Is Suitable

A discretionary trust is often ideal for:

-

Business owners or professionals who need asset protection

-

Families wanting flexibility in distributing income and managing tax

-

Long-term investors planning to grow multiple properties

-

Estate planning and wealth transfer purposes

It may not be ideal if you rely heavily on negative gearing or want to maximise short-term borrowing capacity.

🧠 Trustify Insight

While buying in your personal name is often the simplest option, discretionary trusts provide superior asset protection, tax flexibility, and control — making them one of the most effective long-term structures for serious investors.

However, because trust structures interact differently with lenders, the ATO, and state land tax laws, expert setup and ongoing advice are essential.

At Trustify, we help investors build sustainable structures — balancing protection, flexibility, and finance strategy — so you can grow your property portfolio with confidence.

Information current as of October 2025. Reviewed by the Trustify Business Advisory Team. General information only — not financial or legal advice.

Others

-

-

-

October 20, 2025 Buying Property Under Your Personal Name in Australia: Pros and Cons

-

October 18, 2025 Service Trust Business Structure in Australia

-

October 18, 2025 SPV (Special Purpose Vehicle) Business Structure in Australia